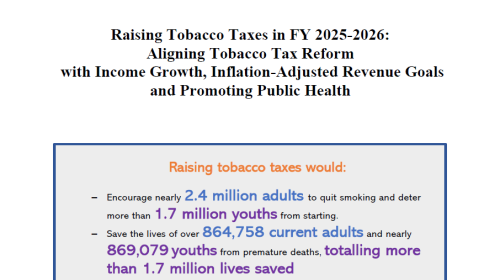

Raising Tobacco Taxes in FY 2025-2026: Aligning Tobacco Tax Reform with Economic Realities and Revenue Goals for Public Health Benefits

35.5% of people 15 years and older in Bangladesh consume tobacco and 18% currently smoke tobacco (GATS, 2017).

Tobacco use in Bangladesh is deadly and costly.[i], [ii]

The current tobacco tax structure in Bangladesh is complex[iii] and is not adequate to discourage tobacco use[iv] and it is not appropriate for optimal revenue collection

The current tobacco tax structure is a complex multi-tiered ad-valorem excise tax which includes large variations in prices and in rate or amount of taxes depending on:

The most effective way to reduce tobacco use is to raise the prices of all tobacco products through tax increases that lower their affordability.

At a minimum, price growth in each tobacco product must outpace the combination of income growth and inflation.

| Recommendation for 2025-2026: Merge low- and medium tier and set MRP to BDT 90 and for premium tier, set MRP to BDT 190 (Table 1). |

Recommendations for cigarette tax system[3]

Table 1

|

|||||||||||||||||||||||||||

Notes: # (colum 2 and 3) prices and excise tax rates as in the revised SRO (Jan 2025). The proposal for FY 2025-2025: No cigarettes should be sold for less than BDT 90, and all cigarettes should be sold at the retail level (consumer price) at the Maximum Retail Price (MRP) to minimize the risk of tax avoidance or evasion.

ECONOMIC JUSTIFICATIONS OF CURRENT PROPOSAL

Merger of Low and Medium Tiers Enhances Efficiency

The proposed merger reduces the complexity of the tax system—a benefit for administration—and prevents smokers from substituting between closely priced low- and medium-tier products. With a uniform MRP of BDT 90, the policy targets the most consumed cigarette segment, which dominates the market.

Alignment with national priorities of Tax-GDP ratio

The proposed increase in cigarette prices offers a significant opportunity to enhance government revenue and improve the tax-to-GDP ratio. Bangladesh’s government has been grappling with fiscal challenges, including a low tax-to-GDP ratio by global standards. By implementing this proposal, the government can generate additional revenue while addressing its budgetary constraints.

Economic Context and Adjusted Affordability

The proposed increases in tobacco taxes are moderate when inflation and income growth are considered. From 2016 to 2022, Bangladesh experienced a substantial 103% increase in average monthly household income, with a corresponding 93% increase in per capita income. In recent years, annual inflation surged to more than 10%. Notably, cigarette prices, particularly in the low-tier cigarette segment, have not kept pace with these economic changes, making these products significantly more affordable (Figure 1). These low prices have helped sustain high consumption and undermines the public health objectives of tobacco tax policy. Moreover, despite experiencing limited income growth due to worsening inequality, low-income individuals faced higher inflation, particularly in food prices. As a result, cigarettes became even more affordable compared to their daily necessities.

In fact, in real terms, this proposal does not go far enough. If the government wishes to return to the same level of affordability as in the pre-COVID period, the MRP of low-tier cigarettes should be set at BDT 88, which is similar to the currently proposed MRP. Figure 1 compares the actual MRPs in the low segment over time (blue bar) to what the price needed to be (orange bar) after adjusting for real income growth and inflation to ensure that cigarettes do not become more affordable. Therefore, the proposed price is not excessively high as it might initially seem without careful consideration.

Revenue Implications of Historical Neglect

The lack of alignment between tobacco tax increases and broader economic changes has had tangible consequences for government revenue. The current tax structure fails to prioritize tobacco revenue growth, as MRP annual adjustments have lagged behind inflation and income growth. This policy inertia has limited the government’s ability to capture the full revenue potential of the tobacco market, representing a missed opportunity to fund essential health, social, and other and development priorities.

Cigarette smokers will not switch to cheaper versions of tobacco, such as biris, as often believed.

Contrary to concerns, data from the past five years show that price increases in the low and medium tiers have not led to significant substitution to bidis. Despite continued increases (though small) in cigarette prices in the lower tier, we have not seen this substitution in sales. In fact, low tier cigarette sales have continued to increase while biris sales have dropped (Figure 2). This evidence underscores that raising prices in these tiers will primarily reduce consumption rather than encourage switching from cigarettes to biris. A recent study[v] found no evidence of such substitution as bidi is now regarded as symbol of low socio-economic status.

Figure 1: actual MRPs vs. inflation and real income adjusted MRPs of low-tier cigarettes

Note: affordability adjusted price means both real income growth and inflation are taken into account. Source: Bangladesh Economic Review, Ministry of Finance, Government of Bangladesh (various years).

Figure 2: The trends of cigarettes and bidis use

If the Government of Bangladesh reforms the current cigarette tax system following the recommendations in FY 2025-2026, it would achieve the following:

A weaker policy is not a good option

Instead of the proposed policy options, the government could opt for a typical increase, such as a BDT 10 increase in all tiers. However, this option would reduce prevalence by only 1.1 percentage points, compared to 2.04 percentage points in the ideal proposal, and generate less than 14 thousand crore additional revenue– resulting in nearly 50% fewer health benefits and 35% less additional revenue. Therefore, the current proposed policy options are a smarter and more effective choice.

Further Tax Recommendations

Additional tax policy changes would further advance tobacco taxation policy which is necessary for Bangladesh to align with global best practices, reduce use and save lives, including:

Bangladesh has committed to achieve tobacco-related targets under the Global Action Plan for the Prevention and Control of NCDs and the Sustainable Development Goals (SDGs) [vi] viii. The proposed cigarette tax reform not only promotes public health by fostering a healthier population but also serves as a powerful tool to generate substantial additional revenue. This revenue can be directed toward financing Bangladesh’s health and development priorities and programs while simultaneously enhancing the sustainability and efficiency of the tax system.

[1] https://www.healthdata.org/research-analysis/health-by-location/profiles/bangladesh

[2] CPI was 50% higher over this period (Source: Bangladesh Economic Review, Ministry of Finance, various issues).

[3] See Shimul, S. N., Hussain, A. G., & Nargis, N. (2022). The Bangladesh Cigarette Tax Simulation Model (BDTaXSiM): A practitioner’s guide for detailed explanation of the process available at https://tobacconomics.org/files/research/813/bangladesh-taxsim-model-technical-note.pdf

[4] Imputed data from 2021 was used due to the absence of updated prevalence data since GATS 2017. However, given the lack of evidence indicating a decline in prevalence—attributed to unchanged affordability and increased cigarette sales—we assumed the current prevalence to remain at 15.1%.

[i] Nargis N, Faruque GM, Ahmed M, Huq I, Parven R, Wadood SN, Hussain AG, Drope J. A comprehensive economic assessment of the health effects of tobacco use and implications for tobacco control in Bangladesh. Tobacco Control. Published Online First: 02 March 2021. doi: 10.1136/tobaccocontrol-2020-056175.

[ii] Hussain AKM Ghulam, Rouf ASS, Shimul SN, Nargis N, Kessaram TM, Huq SM, Kaur J, Sheikh MKA, Drope J. The economic cost of tobacco farming in Bangladesh. International Journal of Environmental Research and Public Health. 2020, 17, 9447; doi:10.3390/ijerph17249447.

[iii] Budget documents of Government of Bangladesh 2011-2021.

[iv] Nargis N, Hussain AKMG, Goodchild M, Quah ACK, Fong GT. A decade of cigarette taxation in Bangladesh: lessons learnt for tobacco control. Bulletin of the World Health Organization. Available online at: https://www.who.int/bulletin/online_first/18-216135.pdf?ua=1.

[v] Shimul, SN, Popova, L., Huang, J. Price Elasticity of Cigarette Demand in Bangladesh: Assessing the Impact of Tobacco Taxes and Graphic Warning Labels Using a Volumetric Choice Experiment. Accepted for SRNT, Louisiana, USA, March 2025.

[vi] United Nations. Transforming Our World: the 2030 Agenda for Sustainable Development. New York, United National General Assembly; 2015.

viii World Health Organization. Health in 2015: From MDGs, Millennium Development Goals to SDGs, Sustainable Development Goals. Geneva, World Health Organization; 2015.

General disclaimer: All reasonable precautions have been taken to verify the information contained in this publication. However, the published material is being distributed without warranty of any kind, either expressed or implied. The responsibility for the interpretation and use of the material lies with the reader.

To read the full document, please click the link Bangladesh Tax Factsheet 2025-2026